How to make your cryptocurrency in 8 steps

-

Written by

Rahul Nambiampurath

Written by

Rahul Nambiampurath - Updated 2026-02-06 18:11:22

Table of content

- Coins are freely exchangeable across any platform, while tokens are only usable within the ecosystem of their original creation.

- So, what exactly is cryptocurrency?

- The upsides of creating your cryptocurrency.

- What is the best approach to producing a blockchain?

- There are several nodes you may employ:

- As a substitute for creating your blockchain, forks are an option

- How do you make your bitcoin fork?

- What is a cryptocurrency fork?

- Are you curious to understand the contrast between a hard fork and soft fork?

- What is a bitcoin fork and when do they occur?

- How to Start a Bitcoin Fork?

- To summarize the process of developing your cryptocurrency

- Biggest Cryptocurrencies That Made It Big: Success Stories

⚡️ How much does it cost to create my cryptocurrency?

Are you looking to create your cryptocurrency? Depending on the features and components you want to include, launching a product or service can cost between $10,000 -$30,000. When making this important decision regarding these elements, it is best to collaborate with a reliable cryptocurrency development company that will help bring your currency to fruition.

⚡️ Is it legal to create a cryptocurrency?

Although it is typically legal to generate cryptocurrencies, some nations and jurisdictions have banned or restricted them. For example, since 2017, China has prohibited collecting money through virtual currencies, and all cryptocurrency transactions have been prohibited since then.

⚡️ Can anyone make a coin?

Although it is possible to create a new cryptocurrency on your own by following any method for creating your own currency, only a group of specialists can select the best technology stack and complete the project in record time.

⚡️How to create an etherium token?

✔️Select the Txn events you want to create.

✔️Set the name, symbol, and decimal number of the token.

✔️Declare the overall sum.

✔️Set the total offer and balances.

✔️Get the owner's balance.

✔️Send tokens to your account.

✔️The process of sending an asset or token is complete when the buyer confirms it.

- Learn your use scenario.

- Determine the consensus method.

- Ensure that the blockchain you're utilizing is sound and safe.

- Node design

- Set the internal structure of your blockchain's database.

- Take care of the API

- Formatting design

- Make sure that your cryptocurrency is legal.

- To ensure success, it's important to understand a few key terms before you get started. Let's review them now!

Coins are freely exchangeable across any platform, while tokens are only usable within the ecosystem of their original creation.

Before we delve into the complexity of creating your own cryptocurrency, let's first define some fundamental terms and establish our facts that all discussions about cryptocurrencies should abide by.

So, what exactly is cryptocurrency?

Let us take a step back and remember the definition of currency: an accounting unit, storage device, as well as medium of exchange. Currency is a valuable asset with dual purposes: it acts as both an accounting unit and medium of exchange for the acquisition, accession, and circulation of products and services.

Cryptocurrency is an innovative digital or virtual currency that utilizes cryptography for safety and security. As any central bank doesn't back it, nor does it have a physical form, cryptocurrencies are completely decentralized and can be used to securely purchase goods and services from the convenience of your home!

The upsides of creating your cryptocurrency.

- Fraud protection – Because cryptocurrency isn't counterfeit able and neither party can reverse prior transactions, fraud is quite difficult.

- Customers may choose for themselves what information sellers should have about them.

- Simply put, cryptocurrency is not affected by interest or transaction costs.

- Bitcoins are immune to the passage of time, public holidays, hours of operation, or the location of buyers and sellers.

- Providing a readily available pool of potential clients – you may now do business with those who do not have access to conventional exchange resources. There are no longer any trading limitations on any of the markets.

- Securing your funds – because cryptocurrency is a decentralized system, there is no Big Brother figure like banks or government agencies that can seize or freeze your assets.

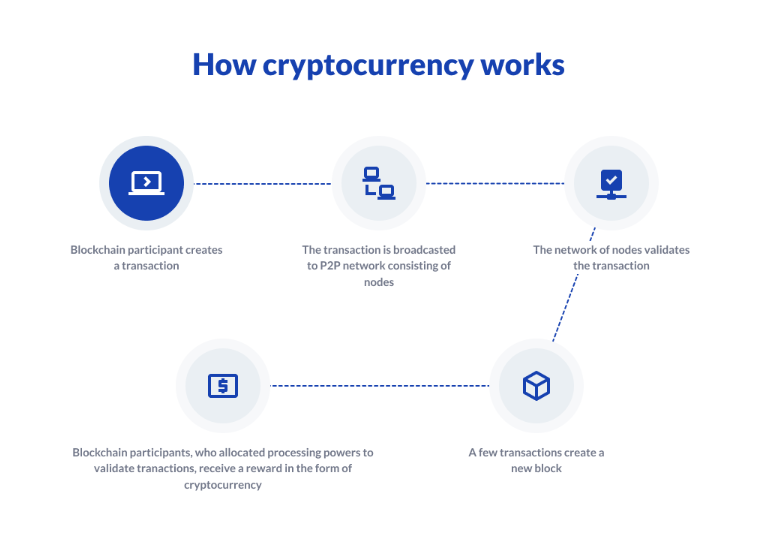

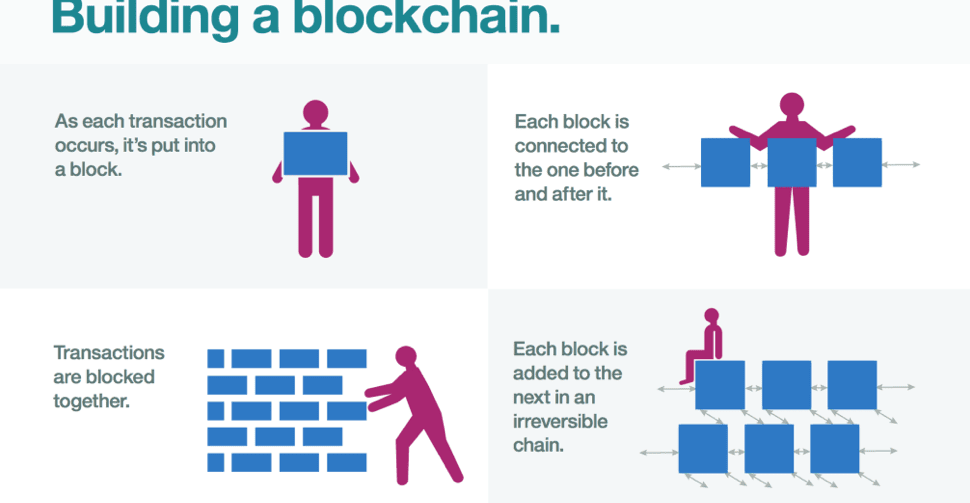

What is the best approach to producing a blockchain?

Now that you comprehend the potential of cryptocurrency to create a secure blockchain for your business, here are the essential steps you must take.

Step 1:Understand your usage scenario.

Is your company interested in the field of smart contracts, data authentication, and verification, or smart asset management? Make your aims clear right from the start.

Step 2: Select a consensus algorithm.

For your blockchain to function, the nodes involved must come to an understanding about which transactions should be accepted as valid and recorded in the chain. A variety of agreement algorithms are available to meet the specific needs of your company. All you have to do is select the one that best suits your business objectives.

Step 3: Choose a blockchain platform.

Depending on the consensus mechanism you want to use, your blockchain platform of choice will be different. To offer you a better sense of what's available, here are the most popular blockchain platforms:

- Etherium (82.70% market share)

- Waves (Waves).

- NEMNxt (NXT).

- Blockstarter

- EOS

- Bitschars 2.0

- coin list

- Fabric hyper ledger

- IBM Blockchain

- Multichain

- HydraChain

- Big chain

- DBOpenchain

- Chain Core

- QuorumIOTA

- KIKIKO

Step 4: Nodes must be designed.

Nodes act as four-legged support systems for a blockchain, keeping it functioning, energy efficient, and safeguarded. A node is any internet-connected device that stores data and then verifies and processes transactions related to the stored data. Without nodes, blockchains wouldn't exist.

There are several nodes you may employ:

- What will they be entitled to in terms of permissions: private, public, or hybrid?

- For optimal performance, will the hosting be cloud-based or situated onsite? Be sure to research and acquire all of the required hardware information, such as processors, memory capacity, disk size – among many other fundamental components.

- Select a primary operating system, such as Ubuntu, Windows, Red Hat, Debian, CentOS, or Fedora.

Step 5: Set the internal architecture of your blockchain network.

Take caution because some settings can't be altered after the blockchain software has already launched. Before making any decisions, it is wise to take your time and reflect upon the following:

- Authorization (who has permission to access the data, initiate transactions, and authenticate them, i.e., construct new blocks).

- The first step in creating a Bitcoin wallet is to choose an address format (how will your addresses appear on the blockchain).

- You can also use the Publishable Key Format field to define key formats (the format of keys that will produce signatures for transactions).

- A few more options and functions are covered below, including the following.

- Reissuing public assets (including the establishment of new units)

- Key management (develop a system for storing and safeguarding private keys that give you access to the blockchain)

- Cryptocurrency transactions require many keys, usually hundreds (if not thousands), so it's crucial to know how many signatures your blockchain requires.

- You can also use atomic swap technologies (a smart contract plan that allows you to exchange several cryptocurrencies without the need for a third party) in your business.

- The parameters of your multi-signature wallet (estimate maximum block size, block mining fees, transaction limits, etc.)

- Assets that are not available in other currencies (set the rules of the native currency issued on the blockchain)

- Deterministic signatures (specify how blockchain participants generating blocks will have to sign them)

- With their expedited performance and effortless implementation, hashes make for excellent authentication and encryption of communications.

Step 6: Make sure you look after the API.

It's also worth noting that each one of the aforementioned platforms has its custom development stack and set of APIs. How to make your cryptocurrency sure you check whether the blockchain software you choose offers out-of-the-box APIs; not all of them do. Don't worry if your platform doesn't have them: there are several trustworthy blockchain API providers to help.

Step 7: Admin and user interface (administrator and user)

Having a well-designed interface creates an efficient way for your blockchain and its participants to communicate by providing all relevant information in one centralized location.

Here's what to think about at this point:

- Web, email, and FTP servers

- External databases

- Web languages are used to create interactive, online applications that require user input and event processing. JavaScript is the most sought-after language due to its ease of learning and quick prototyping abilities. While web development also leverages strong languages such as C++ and Java, they are usually slower than JavaScript due to the absence of garbage collection or dynamic typing.

Step 8: Make your cryptocurrency follow the law.

The legal system is gradually catching up with cryptocurrencies, and you'd better be prepared for any developments by learning about cryptocurrency regulation and future trends.

Develop and improve your blockchain to increase your company's morale and productivity.

You are nearing the finish line! Just a few more steps to take and you will be there. With the progress you have already made, success is within reach. Just think about how you can use new technologies like the Internet of Things, data analytics, artificial intelligence, cognitive service, machine learning, containers, biometrics cloud computing bots, and other amazing advancements to make your blockchain even better.

As a substitute for creating your blockchain, forks are an option

So, what exactly is a bitcoin fork? Comparable to bitcoin, but with a few improvements and adjustments, this new cryptocurrency provides users the same level of security while offering more convenience. Although you may not be able to generate your blockchain for reasons I'll mention later on, you can still utilize forks to develop new coins. With the right approach, success is achievable through an abundance of strategies.

How do you make your bitcoin fork?

Let's take a moment to make sure we're all in agreement by providing a clear definition.

What is a cryptocurrency fork?

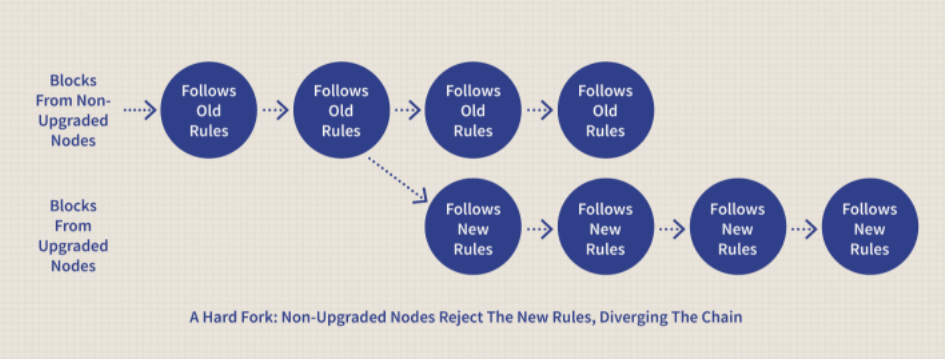

A blockchain fork is a software upgrade, as seen from the perspective of a non-technical user. Every blockchain participant (also known as a full node) relies on the same computer program, which must all use the same version to access a shared registry to authenticate transactions and safeguard the network.

So, when you want to change the program, all full nodes must update to the new version; otherwise, the network will divide into two independent chains–one old and one new. This is called a fork. Now that you know what a fork is, let's examine its operation.

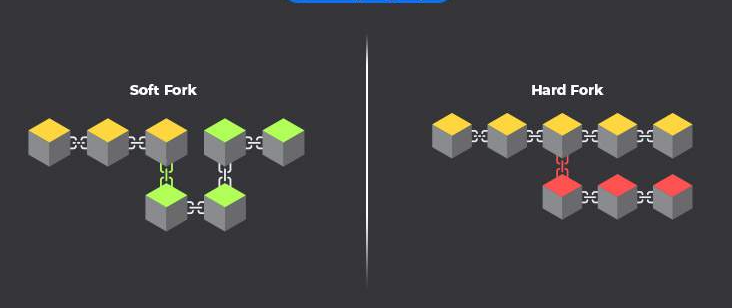

Are you curious to understand the contrast between a hard fork and soft fork?

Hard forks and soft forks are two types of forking.

The software in nodes must be updated to 90% to 95%, and the system will no longer accept nodes with an outdated version.

The difficulties of maintaining manual records are reduced. It simply requires that all nodes upgrade their software, and those who have an earlier version can continue to operate.

What is a bitcoin fork and when do they occur?

Bitcoin forks happen when somebody modifies the protocol for the Bitcoin network. Since Bitcoin uses an open-source protocol, anybody is free to change it however they want to create their currency or improve on the current one by adding new capabilities or solving existing problems.

How to Start a Bitcoin Fork?

Option 1: Use a fork generator.

If you don't have programming abilities, ForkGen may be the ideal answer for you. Anyone can build a unique branch of bitcoins by updating certain parameters and rules using ForkGen, which is an automated fork coin generator that creates new branches of bitcoins.

Option 2. Do it yourself

If you're looking to make a Bitcoin fork with more direct involvement, rather than timidly dipping your toe in the water, take heed of these steps:

- Visit GitHub and download then compile the bitcoin code on your PC.

- The hardware is the most important part. You'll need to restart your computer and reconfigure the bitcoin software.

- Then, publish the code (free) back on Github.

- a website and some documentation are required

If you want to invest your cryptocurrency based on Bitcoin's social and financial capital, forks are worth considering. The following are some examples of successful Bitcoin forks:

- Litecoin

- Bitcoin

- CashBitcoin

- GoldMain

To summarize the process of developing your cryptocurrency

To summarize, you have two options for creating your cryptocurrency: build a blockchain or develop a fork.

To construct a blockchain, you must:

- carefully consider how it can be incorporated into your business plan to maximize its potential benefits.

- Select a mechanism to reach an agreement.

- choose a blockchain technology platform

- create the blocks and characteristics of the blockchain

- You should create an API for tasks completed on your blockchain so that other applications may utilize it.

- develop intuitive and comprehensive administrator and user interfaces

- Take care of the legal aspect of your company.

You can fork the Bitcoin network by:

Forkan, for example, is a program that creates fork coins.

Or:

- Create a bitcoin account by entering the six-digit code from your paper wallet into your Bitcoin app.

- You may also use a piggyback system. Place the stops on the rollers, then run them for a few seconds to stretch out the band's elasticity.

- You'll want to release your solution and keep it updated.

Biggest Cryptocurrencies That Made It Big: Success Stories

Bitcoin

Bitcoin is becoming increasingly well-known, even amongst those unfamiliar with cryptocurrency. As a result, many people use the term “Bitcoin” to refer to all digital assets.

Litecoin

Litecoin is commonly referred to as silver to Bitcoin's gold. Like Bitcoin, it offers speedy transaction confirmation times and rapid block generation rates.

Ethereum

Ethereum is a decentralized platform for smart contracts that are celebrated for being reliable, safe from third-party interference, and fraud-proof.